- All Post

- Uncategorized

- 상품권

- 재테크

- 통신사 소액결제

- 후불결제

- Back

- SKT

- LG U+

- KT

- 아이폰(애플)

April 10, 2024/

토스 후불결제 서비스란 간편 송금 업체 TOSS 앱을 통해 후불결제를 신청 후 한달에 30만원 이내까지 먼저 결제할 수 있는 신용카드…

October 9, 2023/

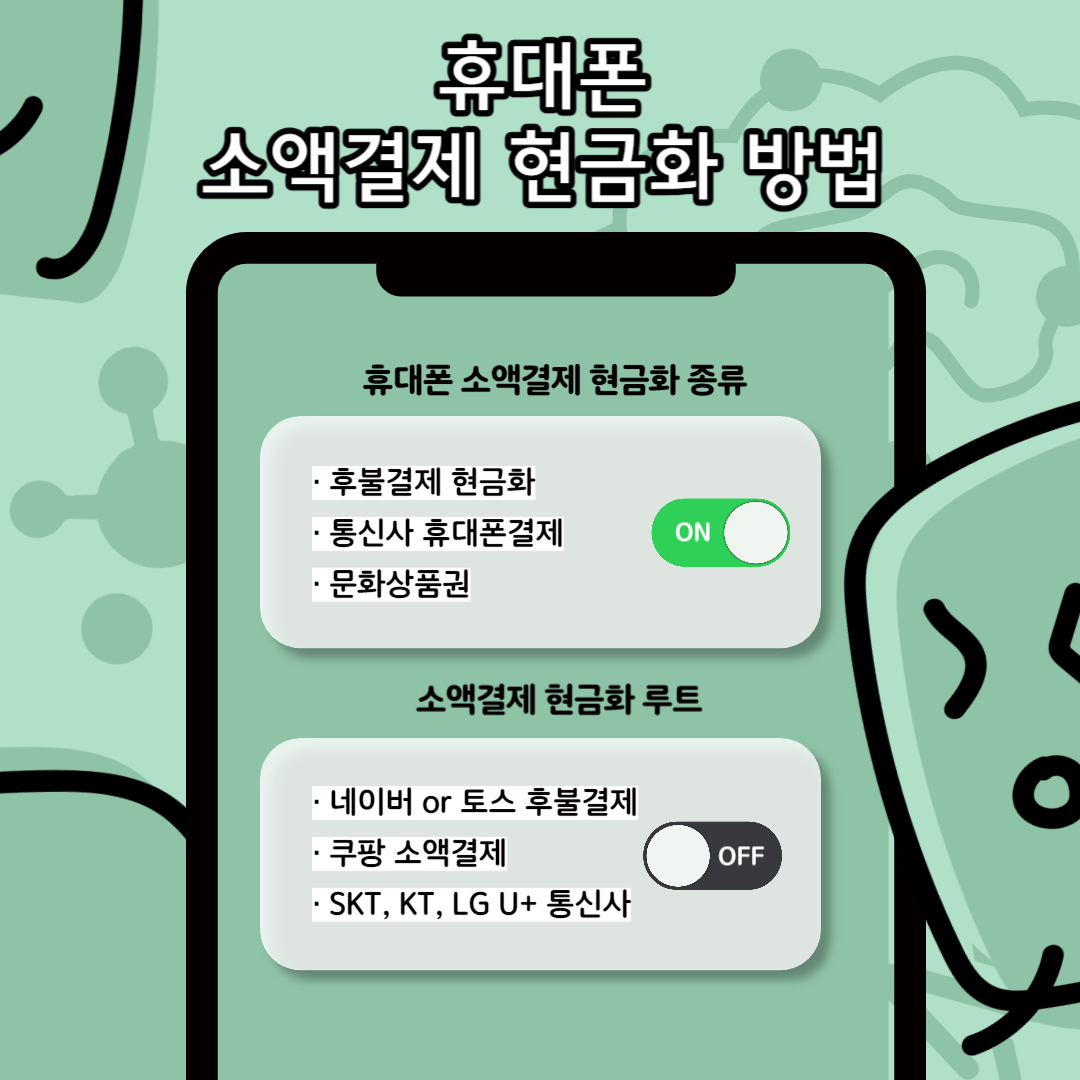

휴대폰 소액결제 현금화는 2단계를 거쳐 콘텐츠 구매 및 현금화가 가능합니다. 첫째, 개통한 핸드폰을 가지고 해당 통신사의 휴대폰 결제 서비스 사용이…

September 6, 2023/

티머니 현금화 방법과 환불 신청 방법에 대해서 알아보겠습니다. 티머니는 최초 전국에서 호환이 가능한 교통카드로 대한민국 교통카드의 상징이라고 볼 수 있습니다.…